A structured settlement is a negotiated financial or insurance arrangement through which a claimant agrees to resolve a personal injury tort claim by receiving part or all of a settlement in the form of periodic payments on an agreed schedule, rather than as a lump sum. As part of the negotiations, a structured settlement may be offered by the defendant or requested by the plaintiff. Ultimately both parties must agree on the terms of settlement. A settlement may allow the parties to a lawsuit to reduce legal and other costs by avoiding trial. Structured settlements are most widely used in the United States, but are also utilized in Canada, England and Australia.

Structured settlements were first utilized in Canada as part of the settlement of birth defect claims arising out of pregnant mothers ingesting Thalidomide. Structured settlements are now used in a wide variety of types of lawsuit settlements such as aviation, construction, auto, medical malpractice and product liability.

You can sell some or all of your structured settlement payments to a factoring company for immediate cash. Although you must first obtain court approval, you have the legal right to cash out your future payments — either in part or in full — to a structured settlement buyer. Depending on the terms of your structured settlement, you may also be able to sell survivor benefits.

Sales of structured settlements begin with a need or want. You want to buy a house or you need to pay off your college loans, for example, but your annuity payments can’t match your wants or needs.

You may wonder, “Can my structured settlement be changed?” It can’t. Once you and the at-fault party reach your terms and a life insurance policy company picks up the annuity, the terms are fixed and finalized. Here is where structured settlement companies, like J.G. Wentworth, come into play.

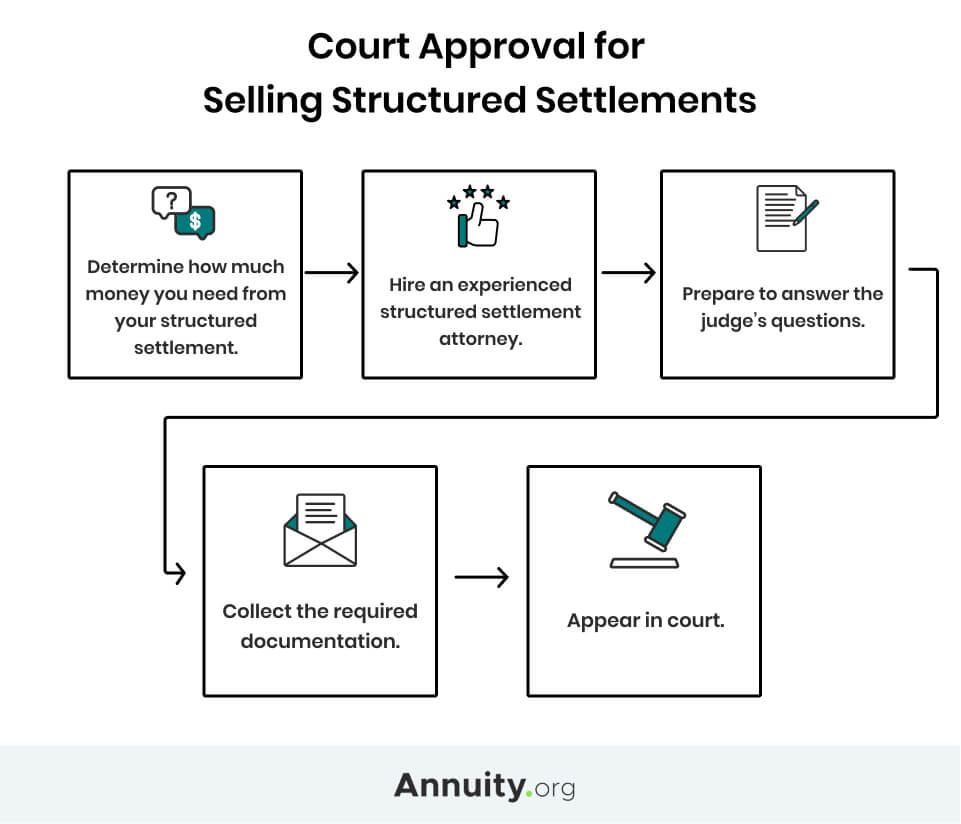

Before you contact a structured settlement company, though, take a few steps backward. Selling a structured settlement works by taking precautions and doing your research, so start with these steps:

Talk to your lawyer Meet with your attorney from your settlement case and ask, “Can I sell my structured settlement?” You may find you’re in violation of the document’s fine print if you transfer your settlement. If your lawyer gives you the thumbs-up, talk with them about why you want to sell all or a portion of your settlement.

Decide your reason to sell A judge evaluates and rules on every structured settlement transfer — it’s the law. If your reason to sell is that you want a new sports car, versus needing to secure a home, a judge will likely rule the transfer isn’t in your best interest. Judges also look into the purchasing company’s history, the amount you’re receiving and any past requests to sell your settlement.

Find your structured settlement company : Sell your structured settlement, or parts of it, the same way you buy a car. Shop around. You’ll probably receive a better price if you don’t choose the first company that gives you a quote. Make sure your broker agrees to pay any fees.

Wait for your court date: Prepare to wait more than a month to two months before meeting with a judge to approve your proposed structured settlement transfer. If you’re pressed for cash, however, a lot of settlement companies provide small cash advances.

Notarize your agreement: Finalize your transfer agreement and receive your funds so you can move on with your life and plans. If you’re pressed for time or want a notary to meet your schedule, mobile notary services are convenient and available nationwide.

1. Selling your structured settlement allows you to convert its periodic payments into a single lump sum of cash.

2. The amount you receive will be less than the total value of the scheduled payments.

3. The structured settlement buyer’s discount rate — along with its fees — will affect how much money you will receive.

4. Structured settlements are thoroughly regulated through both state and federal laws and selling any structured settlement requires a judge’s approval.

If you are thinking about selling your structured settlement payments, we recommend you enlist the help of a trusted attorney or financial advisor with experience in the structured settlement secondary market. They will help you find a credible factoring company with a history of protecting the long-term interests of its clients.

All structured settlement sales require a judge’s approval. The judge will consider the terms of the sale — whether you’re selling some of your payments, a portion of each payment, or your entire structured settlement — and how the sale will affect your long-term financial situation, including the likelihood that you will suffer financial hardship without the regular payments from your structured settlement.

Judges and the courts are responsible for ensuring your best interests are met when selling your payment rights. They can deny a structured settlement based on those grounds. Per the judgment of the court, individuals can be denied the right to sell their payments based on their mental health and age.

Minors, for example, are unable to sell their structured settlements. Courts are fairly protective of a minor’s settlement and will work to protect it and ensure it is used for the child and is available when they turn 18.

Parents, however, can present a case to sell the payment rights to a structured settlement company. The reasons must be beyond compelling, though, and demonstrate that the sale exclusively benefits the child.

The same principle applies to elders or adults assigned guardians because of their mental capacity. If you want to sell their payment rights, it must be to meet the elder or adult’s needs or wants. Courts are often critical of these types of cases to protect the settlement owner, so prepare your case in advance.

The most carefully guarded structured settlements are those that provide for minors. If a child under of the age of 18 received a structured settlement in a personal injury case and his or her circumstances have changed profoundly since the settlement was ordered, a parent or legal guardian may sell the right to future payments, but the burden of proof is high.

Parents or guardians must demonstrate conclusively to the court that there is an immediate need for cash and that the child would be better served by selling the settlement than by receiving future payments.

Can I sell my annuity? Yes, you can sell annuity payments for cash. If an annuity does not fit your financial needs or desires, you can work with an annuity factoring company to sell some or all payments for a lump sum of cash. The most common options are 1) entirety, 2) partial, and 3) lump sum.

1) Entirety – selling an annuity pays out the entire investment as a lump sum and forfeits the annuity holder’s ability to receive future periodic payments. This is the most straightforward way to sell an annuity.

2) Partial – a partial buyout allows the annuity holder to sell a portion of his/her annuity payments and still receive periodic income without forgoing the tax benefits. For example, if the seller needs money immediately, he/she can sell years 1 – 5 of his/her annuity payments in exchange for a lump sum. After those five years have lapsed, the periodic payments will continue. Also, if the seller needs additional funds, he/she can buyout another portion of the remaining payments in exchange for lump sums.

You can start by researching annuity purchasers who can buy all or some of your remaining payments. Next, obtain and compare quotes. Then submit your paperwork to initiate the cash-out process. If your annuity is a structured settlement, there is one additional step: court approval.

Yes, you can sell your annuity payments for cash. In the event your financial needs change and an annuity is no longer meeting your needs,

Selling your annuity provides you with a lump sum of cash. That leaves you free to put a down payment on a house, alleviate larger debt or pay college tuition. It is also important to remember that selling your entire annuity does not mean you will receive the full value of the contract.

Yes, you can sell annuity payments for cash. If an annuity does not fit your financial needs or desires, you can work with an annuity factoring company to sell some or all payments for a lump sum of cash. The most common options are 1) entirety, 2) partial, and 3) lump sum.

The owner is the person who buys an annuity. An annuitant is an individual whose life expectancy is used as for determining the amount and timing when benefits payments will start and cease. In most cases, though not all, the owner and annuitant will be the same person.

A structured settlement follows a court process, and it is a stream of payments determined through negotiations between a plaintiff and a defendant. An annuity is a financial product that guarantees regular payments over time from an insurance company. Contrary to a structured settlement, an annuity itself does not require litigation.

You can sell your structured settlement payments to a reputable factoring company, otherwise known as a purchasing company. It is important to do your research and compare quotes from multiple trustworthy settlement buyers.

Structured annuities are insurance products that are complex, long-term investment vehicles and are subject to risk, including the potential loss of principal. Annuities are intended for retirement investing; therefore, withdrawals made from an annuity before age 59½ may be subject to a 10% IRS tax penalty.

A structured settlement follows a court process, and it is a stream of payments determined through negotiations between a plaintiff and a defendant. An annuity is a financial product that guarantees regular payments over time from an insurance company.

A structured settlement annuity (“structured settlement”) allows a claimant to receive all or a portion of a personal injury, wrongful death, or workers' compensation settlement in a series of income tax-free periodic payments

A settlement agreement establishing the structured settlement will expressly state that the assignment company has all rights of ownership of the annuity. The structured settlement payee only owns the right to receive payments. The payee does not own the structured settlement annuity.

There are three main types of annuities: fixed annuities, fixed-indexed annuities and variable annuities. Variable annuities can be immediate or deferred.

There are five major categories of annuities — fixed annuities, variable annuities, fixed-indexed annuities, immediate annuities and deferred annuities. Which is best for you depends on several variables, including your risk orientation, income goals, and when you want to begin receiving annuity income.

Rate of Return. The rate of return in a low interest rate environment is locked in. It does not increase as interest rates go up.

The main types are fixed and variable annuities and immediate and deferred annuities.

Structured settlements are often used to provide financial compensation for victims of personal injury lawsuits, but they can also be used in other types of legal cases. For example, an insurance company typically makes annuity payments from a structured settlement, which may be made monthly, yearly, or in a lump sum.

A structured settlement is a negotiated financial or insurance arrangement through which a claimant agrees to resolve a personal injury tort claim by receiving part or all of a settlement in the form of periodic payments on an agreed schedule, rather than as a lump sum.

The primary benefits of buying an annuity include principal protection, the potential for guaranteed lifetime income and the option to leave money to your beneficiaries. Some annuities may also be optimized to help pay for long-term care.

One way to think about an annuity is that it provides the opposite type of protection as life insurance. Life insurance provides protection for loved ones when you die; annuities provide a guaranteed lifetime income for yourself, which means you won't outlive your assets or money.

You can sell some or all of your structured settlement payments to a factoring company for immediate cash. Although you must first obtain court approval, you have the legal right to cash out your future payments — either in part or in full — to a structured settlement buyer.

We see most individuals buying annuities starting at age 55, with the average annuity buyer at age 60. These individuals are at the height of their earnings – and their assets. They've accumulated a lot of assets for retirement, and typically, annuities are purchased as part of retirement income planning.

Allowed by the US Congress since 1982, a structured settlement is: A completely voluntary agreement between the injured victim and the defendant. Under a structured settlement, an injured victim doesn't receive compensation for his or her injuries in one lump sum.

Structured settlements are often used to provide financial compensation for victims of personal injury lawsuits, but they can also be used in other types of legal cases. For example, an insurance company typically makes annuity payments from a structured settlement, which may be made monthly, yearly, or in a lump sum.

Structured settlements are meant to provide long-term financial security to the injured party. They are voluntary and agreed upon between the defendant and injured party. If the amount of money is small enough, the wronged party may have the option to receive a lump sum settlement.

Human settlements consist of the five elements nature, man, society, shells and networks, which form a system conditioning the type and quality of our life.

Types of settlement methods. There are two types of settlement methods for e-commerce sites, "automatic settlement" and "designated settlement," which differ in the timing that sales are confirmed. Each is processed differently depending on the settlement method type.

© Copyright 2021-26 GKSchools.com All Rights Reserved.